Farm finances and credit conditions continued to weaken in the second quarter of 2025. According to the Tenth District Survey of Agricultural Credit Conditions, farm income and loan repayment rates in the region declined at a pace similar to recent quarters. Deterioration in agricultural credit conditions was most pronounced in areas more dependent on crop revenues but strong cattle prices continued to support farm finances in some parts of the region. While lenders reported an increase in loan repayment problems, the majority of issues remained minor and recent assistance related to the American Relief Act was expected to provide modest support to producers.

The outlook for the U.S. farm economy remained subdued through mid-2025 alongside relatively low crop prices. Weak profit margins for key crops have reduced working capital for many producers and led to increased loan demand. Financing costs also remained elevated alongside relatively high interest rates. Agricultural real estate values declined slightly through the first half of 2025 but remained strong, providing some support to farmer balance sheets.

Section 1: Farm Finances and Credit Conditions

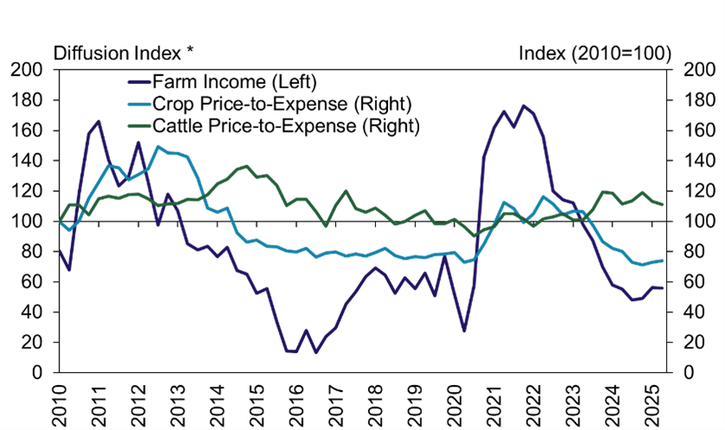

Farm financial conditions in the Tenth District tightened gradually alongside weak crop prices. According to survey respondents, the pace of decline in farm income was similar to recent quarters (Chart 1). Despite ongoing strength in the cattle sector, farm finances in the region have tightened considerably as profit opportunities for crop producers remained limited.

Chart 1: Tenth District Farm Income and U.S. Farm Price-to-Total Production Expenses

*The index numbers are computed by subtracting the percentage of respondents who responded "lower" from the percentage who responded "higher" and adding 100.

Sources: USDA, Haver Analytics and staff calculations

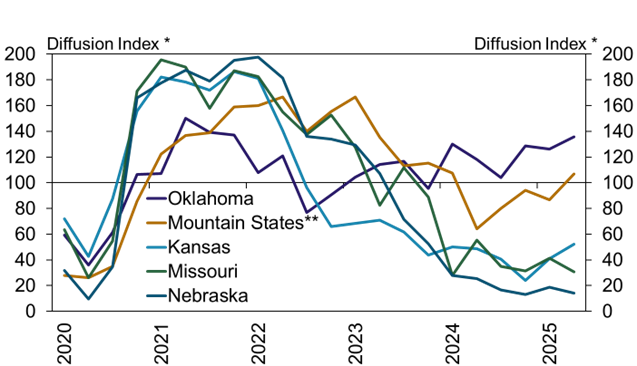

Farm income deteriorated most in areas more heavily concentrated in crop production. The share of lenders that reported farm income was lower than a year ago was highest in Nebraska, Missouri, and Kansas where corn and soybeans comprise a comparatively larger share of aggregate state farm revenues (Chart 2). In Oklahoma, however, half of respondents indicated that farm income was higher than the same time last year.

Chart 2: Farm Borrower Income by State

*The index numbers are computed by subtracting the percentage of respondents who responded "lower" from the percentage who responded "higher" and adding 100.

** Mountain States include Colorado, northern New Mexico and Wyoming, which are grouped because of limited survey responses from each state.

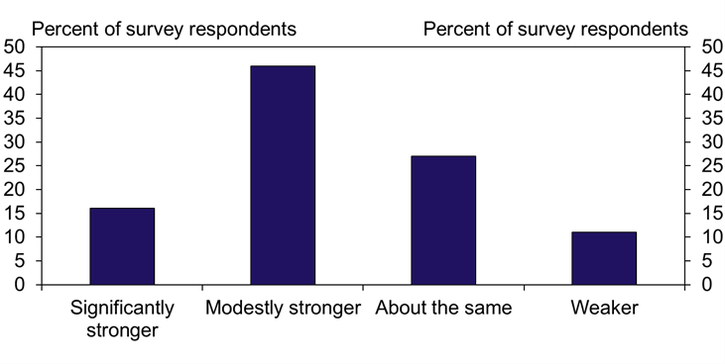

Producers who are primarily renters could be more exposed to financial pressures. About 60% of survey respondents answered that the financial conditions of majority owner-operators were at least modestly stronger than majority renter-operators (Chart 3). Renters have a more limited ability to leverage strength in farmland valuations to improve working capital positions and could be more challenged by weak crop profits.

Chart 3: Comparison of Owner-Operator vs. Renter-Operator Financial Conditions

Note: Respondents answered the following question: How do overall financial conditions for majority owner-operators compare with overall financial conditions for majority renter-operators in your lending area?

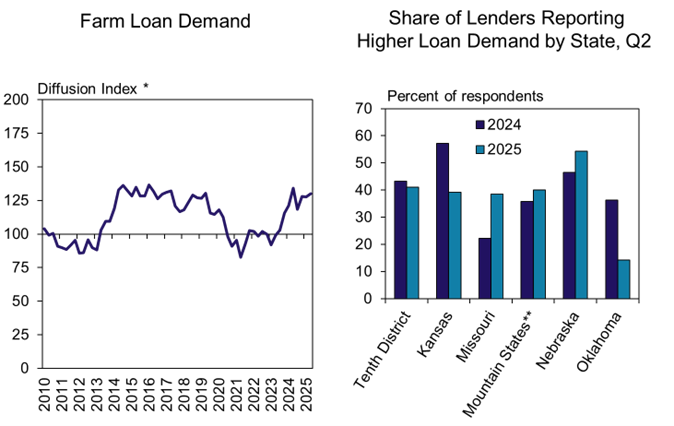

As financial conditions continued to tighten, demand for credit increased steadily. Much like farm income, the pace of increase in demand for non-real estate farm loans was also similar to recent quarters (Chart 4, left panel). The share of respondents reporting that demand was higher than a year ago increased most notably in Missouri but declined notably in Oklahoma (Chart 4, right panel).

Chart 4: Tenth District Farm Loan Demand

*The index numbers are computed by subtracting the percentage of respondents who responded "lower" from the percentage who responded "higher" and adding 100.

** Mountain States include Colorado, northern New Mexico and Wyoming, which are grouped because of limited survey responses from each state.

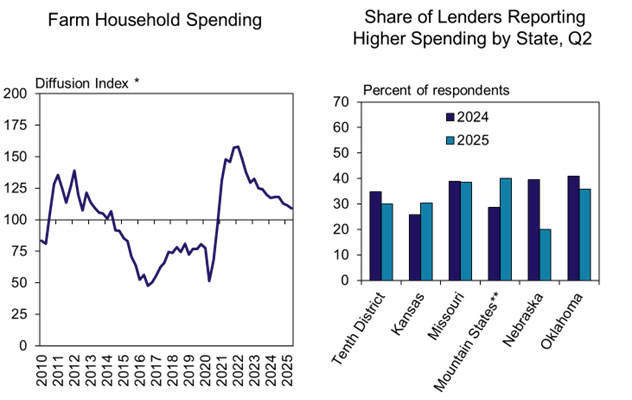

Upward pressure on household expenses eased, but likely continued to challenge many borrowers. The pace of increase in farm borrower household spending slowed from previous quarters, but some lenders commented that financial pressures from elevated living costs persisted (Chart 5, left panel). The share of respondents that reported household spending was higher than a year ago was near 30% in most states (Chart 5, right panel).

Chart 5: Tenth District Farm Household Spending

*The index numbers are computed by subtracting the percentage of respondents who responded "lower" from the percentage who responded "higher" and adding 100.

** Mountain States include Colorado, northern New Mexico and Wyoming, which are grouped because of limited survey responses from each state.

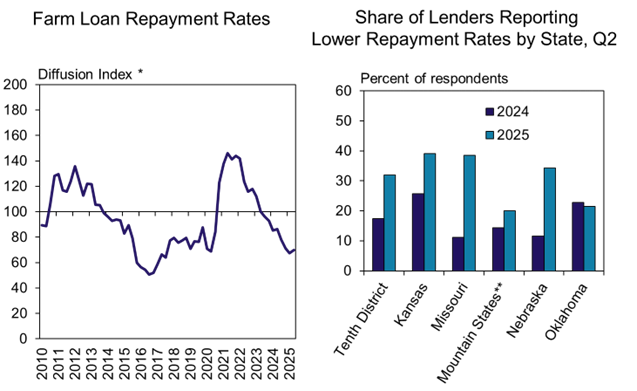

With further softening in farm finances, credit conditions deteriorated steadily. Farm loan repayment rates declined at a pace similar to recent quarters and comparable to the period between 2017-2019 (Chart 6, left panel). The share of lenders that reported lower repayment rates increased to more than 30% in all states except Oklahoma and the Mountain States (Chart 6, right panel).

Chart 6: Tenth District Farm Loan Repayment Rates

*The index numbers are computed by subtracting the percentage of respondents who responded "lower" from the percentage who responded "higher" and adding 100.

** Mountain States include Colorado, northern New Mexico and Wyoming, which are grouped because of limited survey responses from each state.

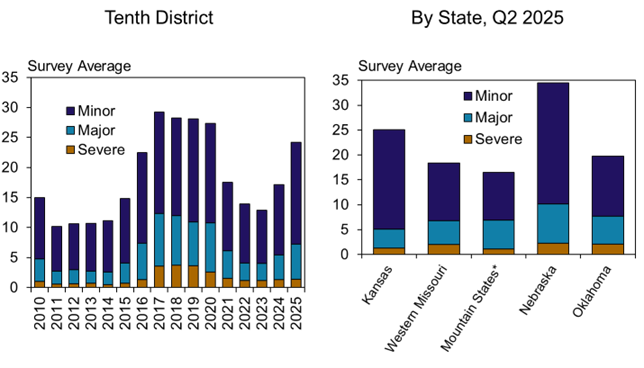

Loan performance weakened alongside recent deterioration in financial conditions, but most repayment issues remained relatively minor. On average across the region, less than 10% of farm loan balances had major or severe repayment problems while about 15% had minor troubles (Chart 7, left panel). Repayment issues were most pronounced in Nebraska where lenders reported, on average, that about 35% of loans had at least minor difficulties (Chart 7, right panel).

Chart 7: Degree of Farm Loan Repayment Problems, Q2

Note: Respondents answered the following question: Please indicate the percentage of the dollar amount of your bank's farm loan portfolio that currently falls within each of the following repayment classifications (None, minor, major or severe).

*Mountain States include Colorado, northern New Mexico and Wyoming, which are grouped because of limited survey responses from each state.

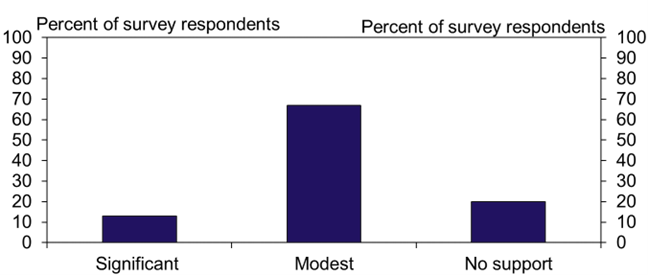

The recent distribution of assistance from the American Relief Act may ease some financial pressure for borrowers in 2025. Nearly 70% of lenders in the District anticipated economic and supplemental disaster assistance would provide modest support to farm finances and another 10% thought the support would be significant (Chart 8). The remaining 20% of respondents expected no support or were uncertain.

Chart 8: Level of Support to Farm Finances Expected from American Relief Act, Q2 2025

Note: Respondents answered the following questions: What level of support do you expect financial aid related to the American Relief Act (ECAP, ELRP, and other supplemental disaster assistance) to provide for farm income and credit conditions in your lending area?

Section 2: Interest Rates and Farmland Values

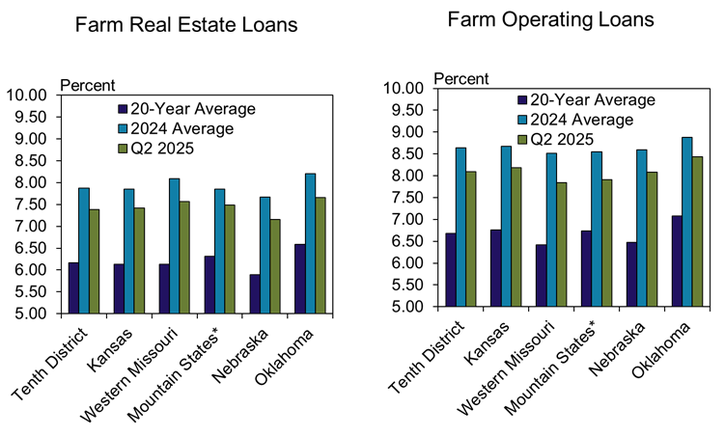

As credit conditions tightened and loan demand grew gradually, interest rates on farm loans remained above recent historic averages. Average interest rates charged on farm real estate and operating loans were more than 50 basis points lower than in 2024, but remained more than 125 basis points above the average of the past 20 years (Chart 9). The slight decline over the past several months was similar across all states in the region for all types of loans.

Chart 9: Tenth District Average Farm Loan Interest Rates

*Mountain States include Colorado, northern New Mexico and Wyoming, which are grouped because of limited survey responses from each state.

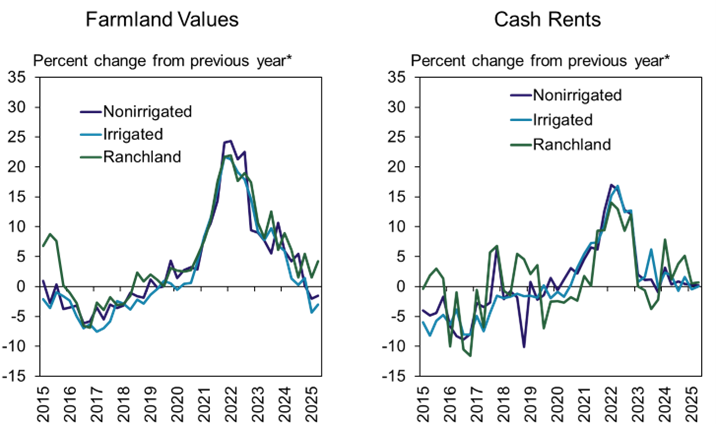

Farmland values remained strong, but declined slightly alongside weaker farm finances and relatively high interest rates. According to lenders, the value of cropland in the region declined by about 2% from a year ago while ranchland increased about 4% (Chart 10, left panel). Similar to recent months, cash rents on all types of land were nearly unchanged from a year ago (Chart 10, right panel). Despite modest declines in recent months, the average value of nonirrigated cropland remained about 70% higher than in 2020 and more than 300% higher than in 2010.

Chart 10: Tenth District Farmland Values and Cash Rents

*Percent changes are calculated using responses only from those banks reporting in both the past and the current quarters

Banker Comments Q2 2025

“The strong cattle market is supporting diversified farmers and keeping them afloat. Farmers with mostly wheat are struggling mostly due to very low commodity prices and constant increasing of input costs.”

“Low grain prices are hurting farm cash flows.”

“Broad inflation, high input costs, tariffs and dry moisture conditions will impact agriculture in 2025.”

“Less ag liquidity in 2025 has caused an increase in loan demand for operating expenses.”

“Nearly all of our farm customers are realizing significant losses in working capital. However, they still have significant net worth and reasonable debt to asset ratios.”

“If the current grain market environment does not change, our farm customers are in for another rough year; likely to continue losing liquidity.”

“Low grain prices, with elevated input costs, including interest and family living, are contributing to financial hardship.”

“In our area, higher farm income is mostly attributed to higher cattle prices.”

“We actually have too much rain for this area that is affecting the ability to harvest wheat, and the quality will be reduced.”

A total of 105 lenders responded to the Second Quarter Survey of Agricultural Credit Conditions in the Tenth Federal Reserve District—an area that includes Colorado, Kansas, Nebraska, Oklahoma, Wyoming, the northern half of New Mexico and the western third of Missouri. Please refer questions to Ty Kreitman at 1-800-333-1040.

The views expressed are those of the authors and do not necessarily reflect the positions of the Federal Reserve Bank of Kansas City or the Federal Reserve System.

Author