A prolonged downturn in the agricultural economy continued in the second quarter of 2017, but recent data suggest conditions in the farm sector may be stabilizing. Although farm income and farm real estate values continued to decline, and credit conditions weakened further, the pace of deterioration has slowed. With the fall harvest approaching, agricultural lenders and borrowers remain concerned about prospects for the farm economy in the Federal Reserve’s Tenth District, particularly in regions with limited potential for high crop yields. However, bankers were generally less pessimistic about economic conditions in the farm sector in the second quarter than in each of the past two years.

Data

Credit Conditions | Fixed Interest Rates | Variable Interest Rates | Land Values

Agricultural Credit Conditions

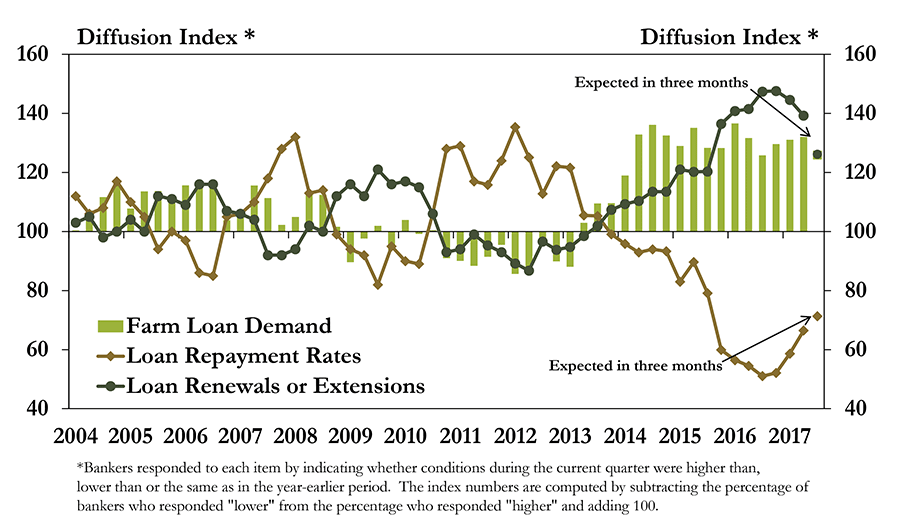

Agricultural credit conditions weakened further in the second quarter, but the pace of deterioration has slowed. Although the rate at which farm loans are being repaid continued to decrease, the change from a year ago was not as sharp as in recent years (Chart 1). Only 37 percent of bankers in the Tenth District reported a decrease in repayment rates from a year ago, the lowest share since mid-2015. An even smaller share expected repayment rates to decline again in the third quarter. Similar to the past three years, demand for farm loans at agricultural banks in the District continued to rise, but at a slightly slower pace than in recent quarters.

Chart 1: Tenth District Credit Conditions

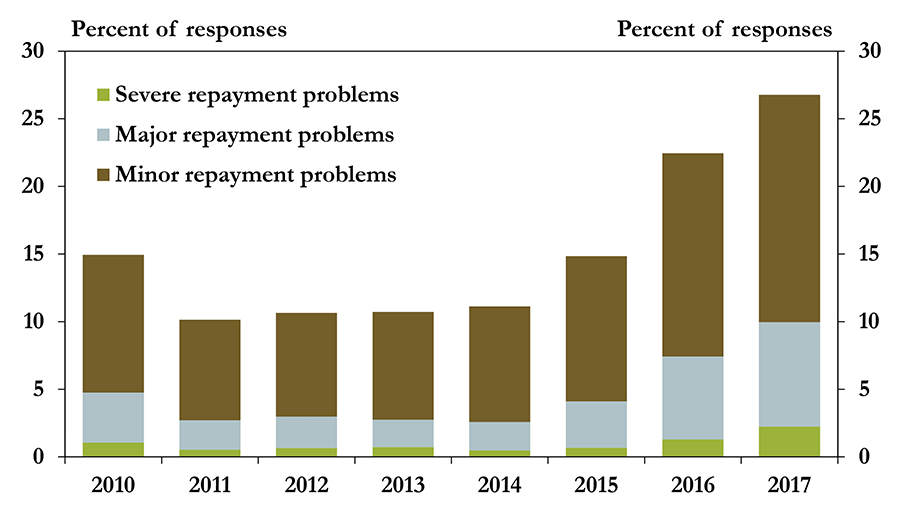

The severity of loan repayment problems also increased, but not as sharply as a year ago. In the second quarter, 27 percent of bankers reported “minor repayment problems,” up from 22.5 percent a year ago (Chart 2). However, the change from 2015 to 2016, an increase from 14.8 percent to 22.5 percent, was more significant. Moreover, only 2.2 percent of bankers reported “severe repayment problems” in the second quarter.

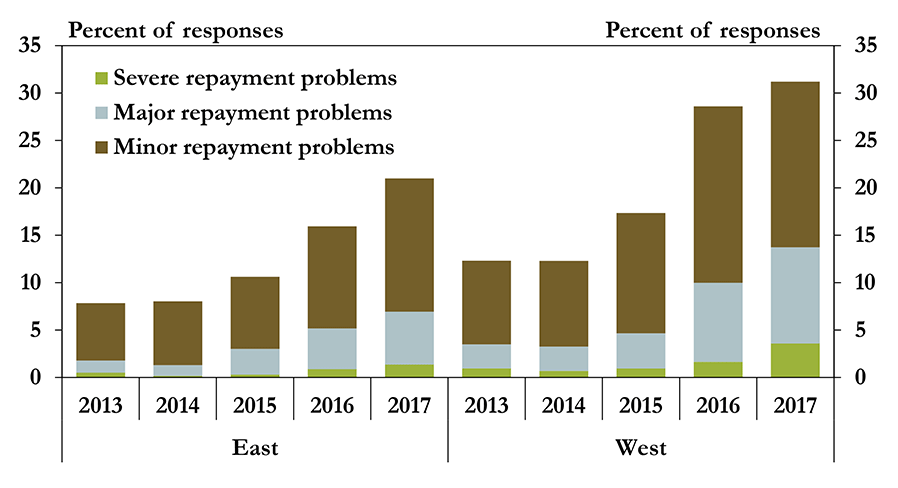

Consistent with the recent trend, repayment problems also remained less severe in the eastern portion of the Tenth District. Strong crop yields last fall in the eastern third of the District have boosted cash flow in recent months, and bankers in the region reported fewer concerns about loan repayments. Whereas 31.5 percent of bankers in the western portion of the District reported at least “minor repayment problems” in the second quarter, only 21.3 percent reported problems in the eastern portion.

Chart 2: Farm Loan Repayment Problems, Second Quarter

Chart 3: Farm Loan Repayment Problems, Second Quarter

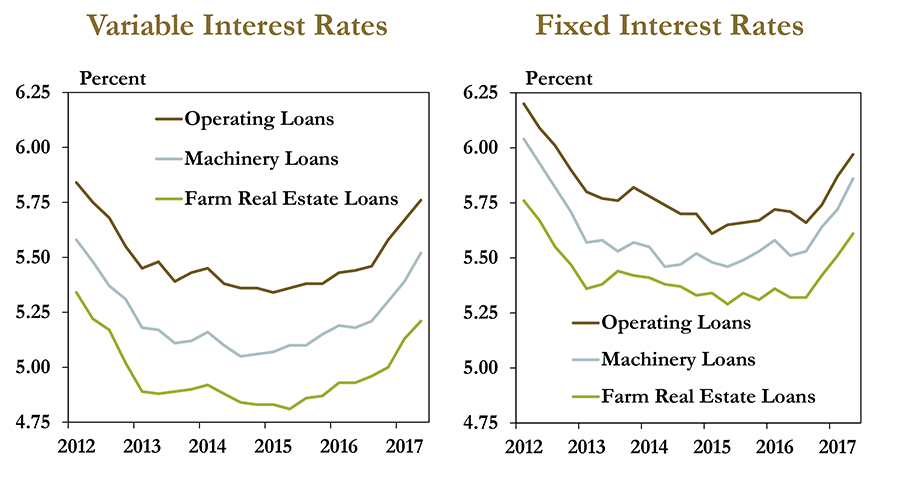

As repayment rates have continued to weaken and benchmark interest rates have risen, bankers further increased interest rates on farm loans. Interest rates on variable rate operating loans increased to 5.8 percent in the second quarter, the highest in five years (Chart 4). Interest rates on other farm loans, including loans for machinery and real estate, increased at a similar pace. The recent increases in rates may be in response to heightened risk in the farm sector, but also may be attributed partially to movements in short-term interest rates. The federal funds rate, for example, has increased in 2017 to an effective rate of more than 1.0 percent.

Chart 4: Average Farm Loan Interest Rates

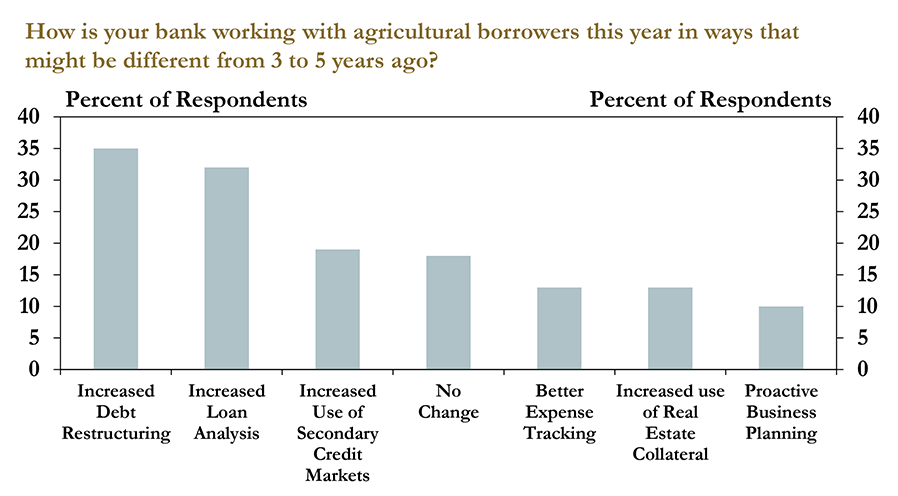

In addition to making slight increases in interest rates, bankers have taken other steps to manage risk in their agricultural loan portfolios. Compared with bank practices of several years ago, the primary changes have been an increased use of debt restructuring and increased loan analysis (Chart 5). About 35 percent of bankers noted they had increased debt restructuring activity to provide additional liquidity in the short term. Nearly 30 percent of bankers also reported an increase in loan analysis. In addition, numerous bankers reported an increase in the use of secondary credit markets, better expense tracking and increased collateral requirements.

Chart 5: Changes in Ag Lending Practices

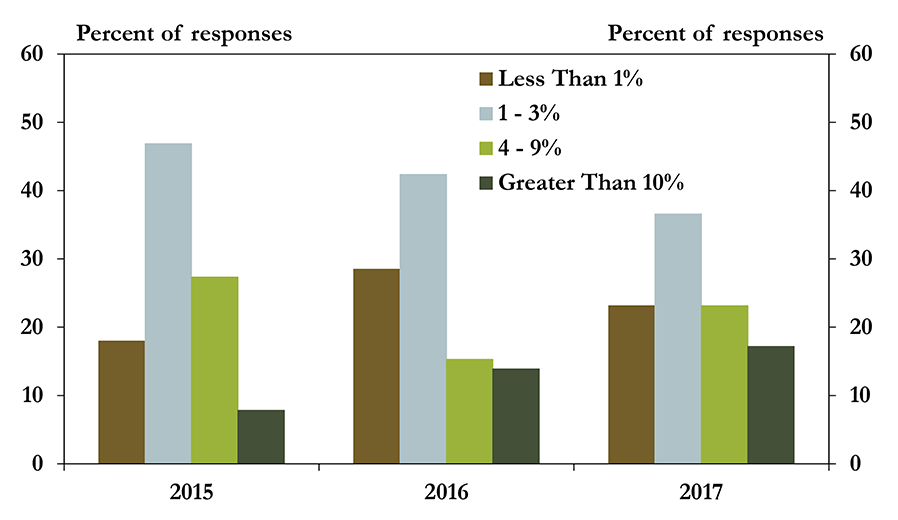

Bankers also were slightly more cautious than a year ago in approving new loan applications. In the second quarter, about 17 percent of bankers reported that they denied at least 10 percent of all new farm loan requests, up from the previous two years (Chart 6).

Chart 6: Percent of Farm Operating Loan Applications Denied, Second Quarter

Farm Income

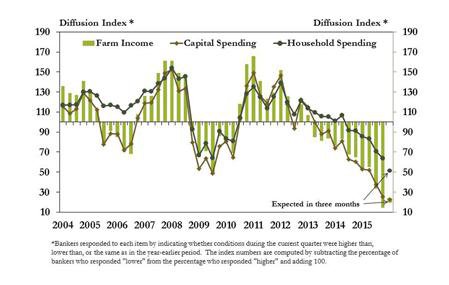

Similar to credit conditions, income in the farm sector continued to weaken but not as rapidly as in recent years. Although 57 percent of bankers reported lower farm income in the second quarter, it was the smallest share in two years (Chart 7). Less than half of respondents expected farm income to drop again in the third quarter. Capital spending and household spending continued to decline from a year ago, but the pace of the declines also softened in the second quarter.

Chart 7: Tenth District Farm Income and Spending

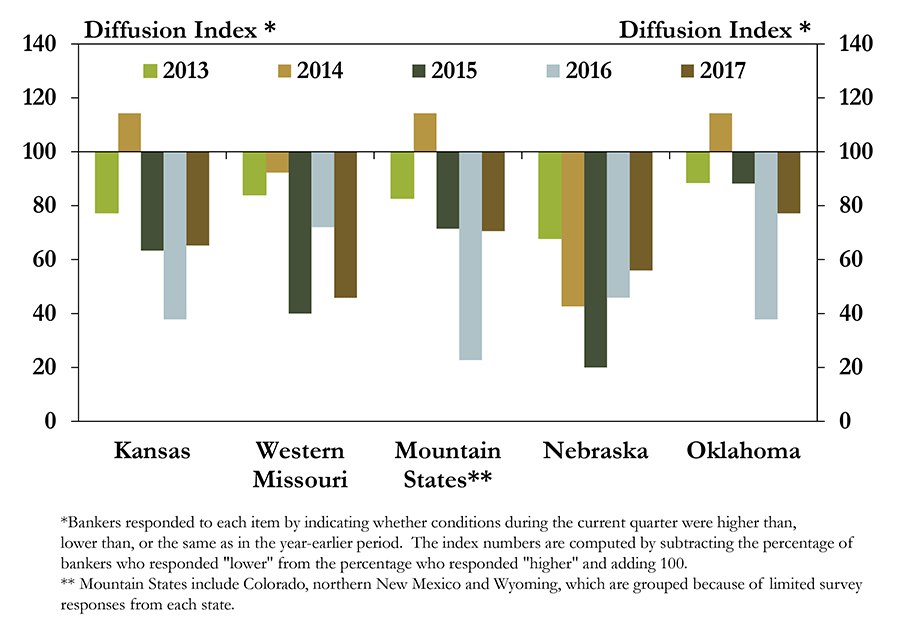

Bankers in most District states expected the decline in farm income to be slower in 2017 than in 2016. In 2015, Nebraska bankers had expected a significant decline in farm income, but the decline in the last two years has eased. Similarly, income declines this year in Kansas, Oklahoma and the Mountain States were expected to be less pronounced. Only in western Missouri, where record harvests boosted incomes last year, bankers expected farm income to fall more rapidly than a year ago (Chart 8).

Chart 8: Expected Tenth District Farm Income, Second Quarter

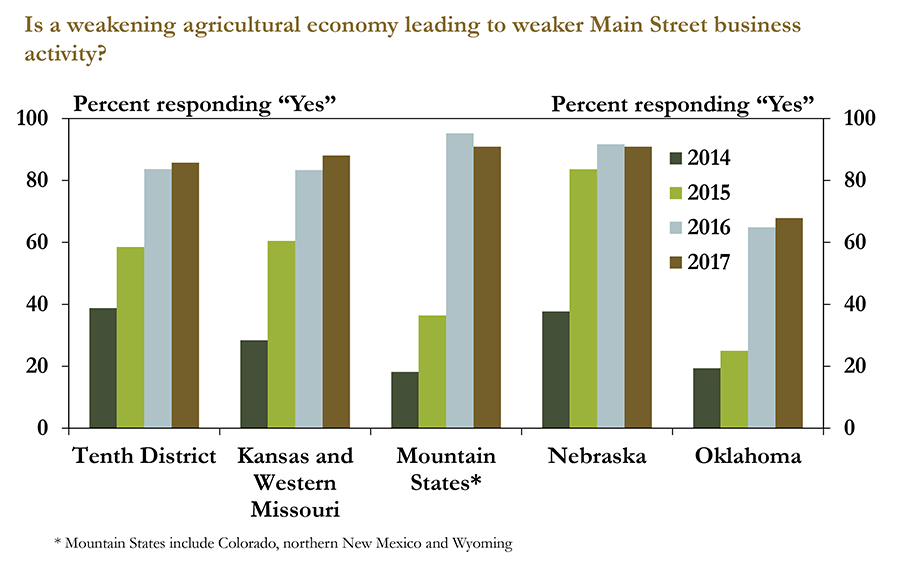

Despite some signs of stabilization in the District farm economy, prolonged weakness has continued to dampen business activity on Main Street in rural areas. In fact, in line with a year ago, 85 percent of bankers reported that the weakening farm economy has led to weaker business activity (Chart 9). Bankers in Oklahoma were slightly less pessimistic about the spillover from agriculture to Main Street, but a majority of respondents in all District states indicated the downturn in the farm economy was affecting business activity outside of agriculture in their lending regions.

Chart 9: Effect of Current Agricultural Economy on Main Street Business Activity

Farmland Values and Cash Rent

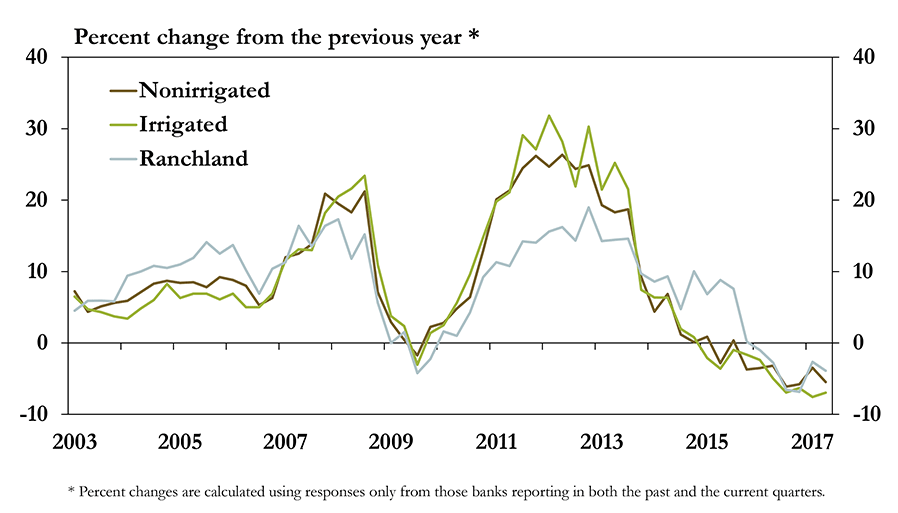

Farmland values continued to trend lower alongside the reductions in farm income and weaker credit conditions, but the changes have remained modest. For the sixth consecutive quarter, the value of cropland and ranchland in the District decreased from a year ago (Chart 10). Similar to recent quarters, the value of irrigated cropland, nonirrigated cropland and ranchland decreased 7 percent, 5 percent and 4 percent, respectively.

Chart 10: Tenth District Farmland Values

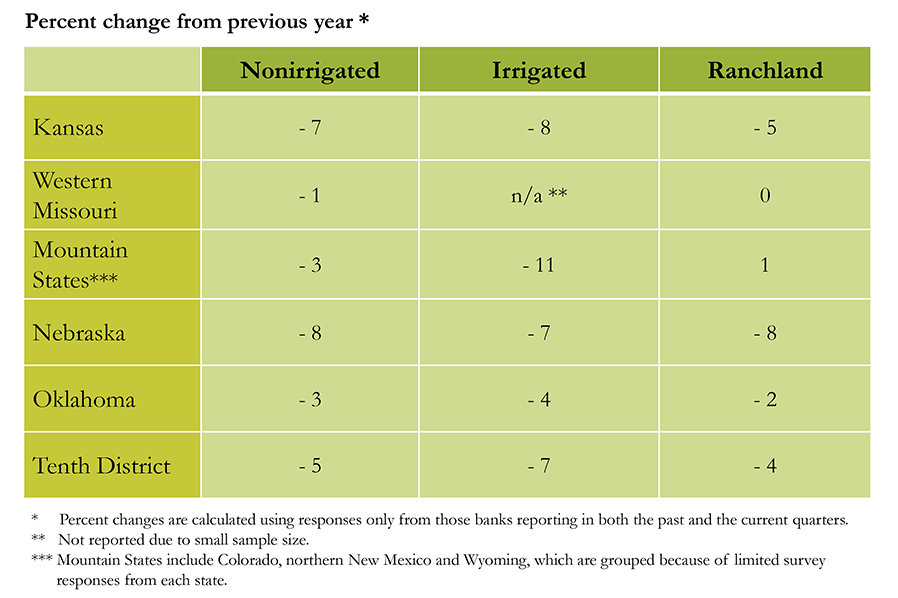

The value of farmland also declined in each District state for most types of land. Most notably, the value of irrigated cropland decreased 11 percent in the Mountain States and continued to decline at a modest pace in Nebraska and Kansas (Table). Ranchland values also fell further in most states but were flat in western Missouri and the Mountain States. Recent wildfires in northeast Colorado and some drought concerns in the broader region have likely contributed to more stable ranchland values in the Mountain States as available pastureland was sold for a premium.

Table: Tenth District Farmland Values Gains by State, Second Quarter 2017

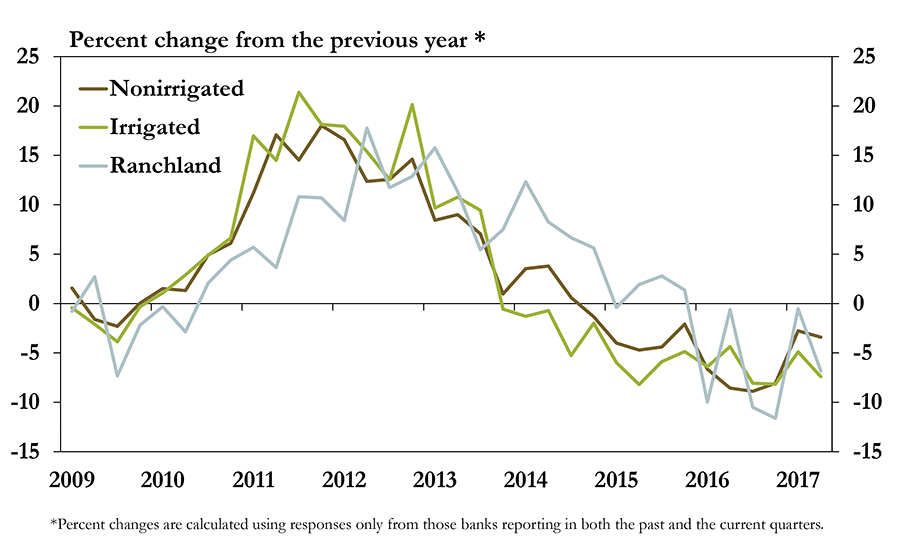

Similarly, cash rents also declined at a modest pace as farm income continued to weaken. Consistent with changes in the value of farm real estate, cash rental rates for cropland and ranchland have declined for six consecutive quarters (Chart 11). Cash rents for irrigated cropland decreased about 7 percent in the second quarter, a pace that has been maintained for the past two and a half years. Cash rents for nonirrigated cropland and ranchland also decreased at a pace generally consistent with the average of recent years.

Chart 11: Tenth District Cash Rents

Conclusion

The outlook for the farm economy in the Tenth District remained subdued in the second quarter, but changes in coming months may not be as severe as in recent years. Following a sharp drop in crop prices in 2013, income in the farm sector also dropped rapidly, agricultural credit conditions deteriorated, and farmland values cooled. However, agricultural commodity prices have steadied recently, and have rebounded in the cattle sector. As prices have stabilized, albeit at a relatively low level, the pace of declines in the farm sector also may be less pronounced than in recent years.

The views expressed in this article are those of the authors and do not necessarily reflect the views of the Federal Reserve Bank of Kansas City or the Federal Reserve System.

Author