Prospects for farm income and agricultural credit conditions rebounded sharply in the fourth quarter of 2020. The average price of corn, soybeans and wheat increased more than 20% from the previous quarter, and reached six year highs in December. Livestock prices, while still less than a year ago, also improved from lows reached earlier in the year. Government payments provided broad support through the year and, together with recent price increases, the near-term outlook for the farm sector improved dramatically.

Data

Credit Conditions | Fixed Interest Rates | Variable Interest Rates

Land Values

Farm Income

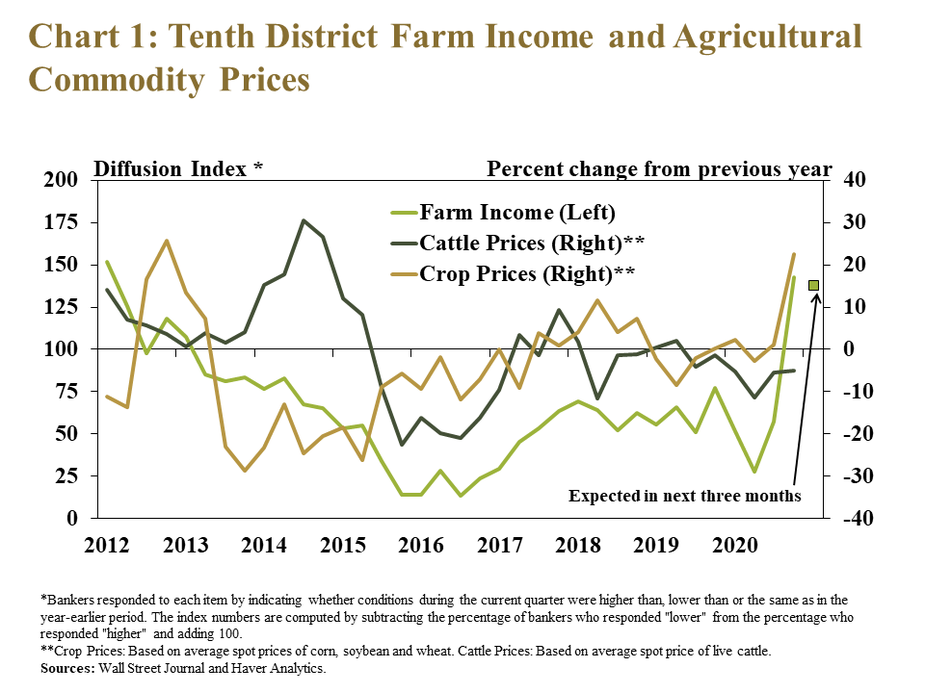

After nearly eight years of deterioration, farm income across the Tenth District rebounded in the fourth quarter alongside sharp increases in crop prices. A majority of respondents reported that incomes of farm borrowers were higher than a year ago for the first time since 2012 (Chart 1). This was a clear contrast to recent years in which a majority of bankers consistently reported steady declines in farm income.

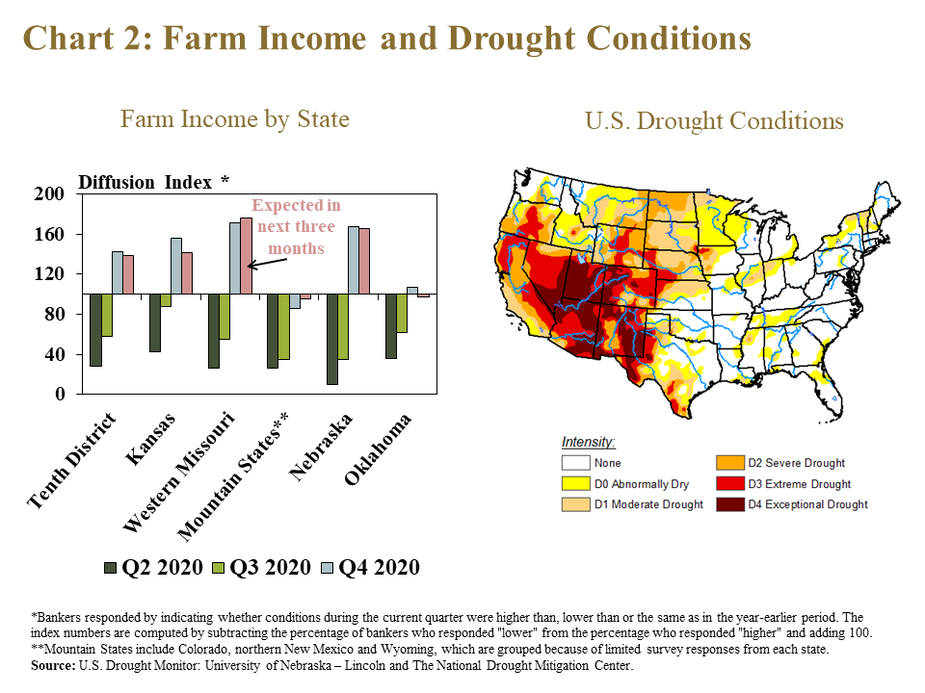

Areas of the region more dependent on livestock revenues and exposed to severe drought were somewhat less optimistic about farm income in the fourth quarter. For example, the share of bankers that reported higher income than a year ago was far smaller in Oklahoma and the Mountain States, where drought conditions intensified and less revenue is attributed to crop production (Chart 2). In fact, about 30% of respondents in those states indicated that incomes were lower than a year ago, compared with only 8% in all other states.

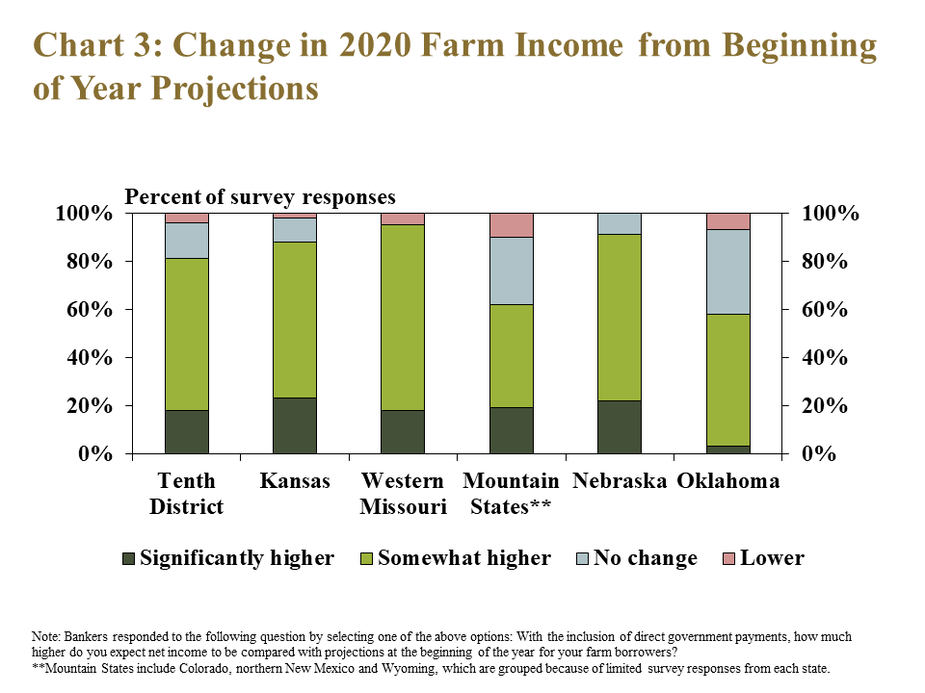

With a recent boost in profit opportunities and strong support from government aid, the financial outcome for borrowers in 2020 was notably better than what was expected earlier in the year. About 80% of bankers expected farm incomes for the entire year would be higher than initially projected in early 2020 when factoring in government payments; and nearly 20% expected the increase to be significant (Chart 3). Compared with other states in the District, the turnaround in farm income was less pronounced in Oklahoma and the Mountain States.

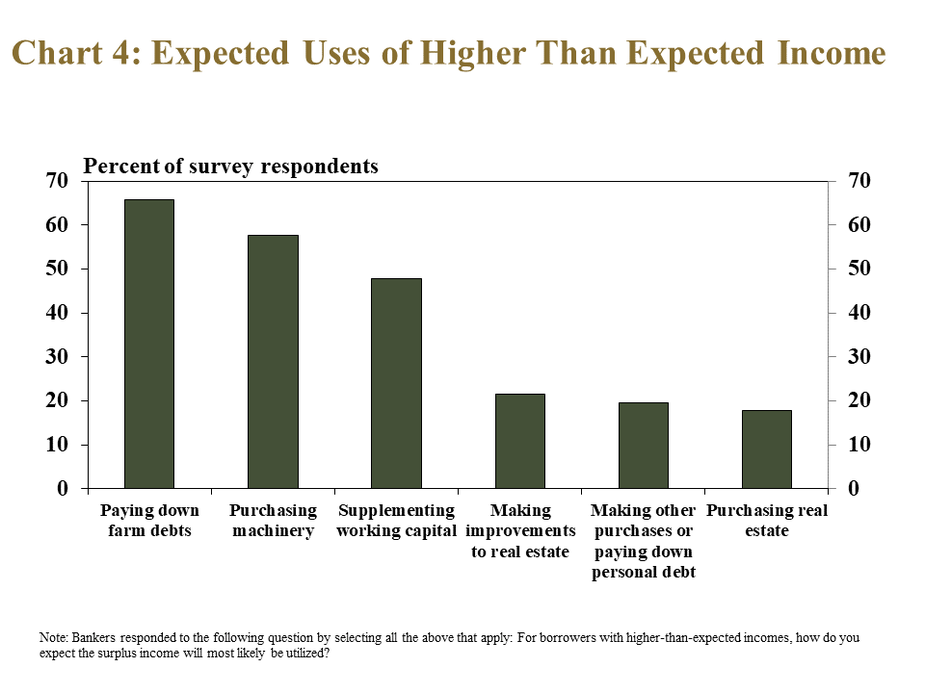

Agricultural lenders expected farmers to strengthen their balance sheets and make capital purchases with incomes larger than initially expected. About 60% of respondents listed paying down farm debts or machinery purchases as likely uses of extra income (Chart 4). Slightly less than half indicated improving working capital also would be a priority and a smaller share anticipated other types of spending.

Credit conditions

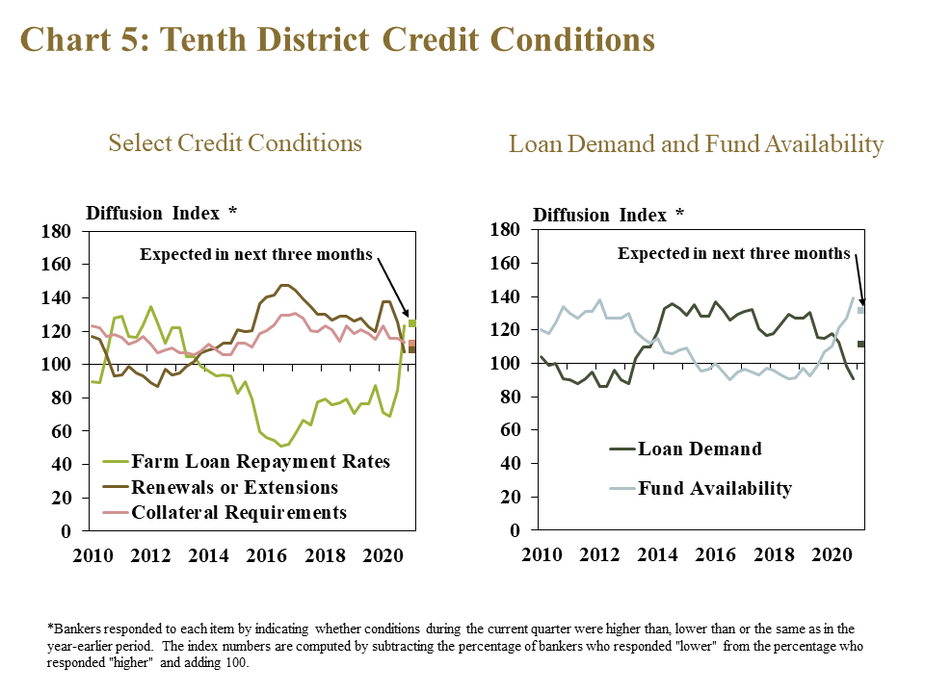

Along with better prospects for farm income, credit conditions in the region also improved following several years of steady deterioration. About a third of bankers reported that farm loan repayment rates were higher than the previous year, the largest share since 2012 (Chart 5). Renewals or extensions increased at the slowest pace since 2014 and tightening of credit standards also slowed. At the same time, the District measure of loan demand retracted for the first time since 2013 and fund availability expanded at the fastest pace since 2012.

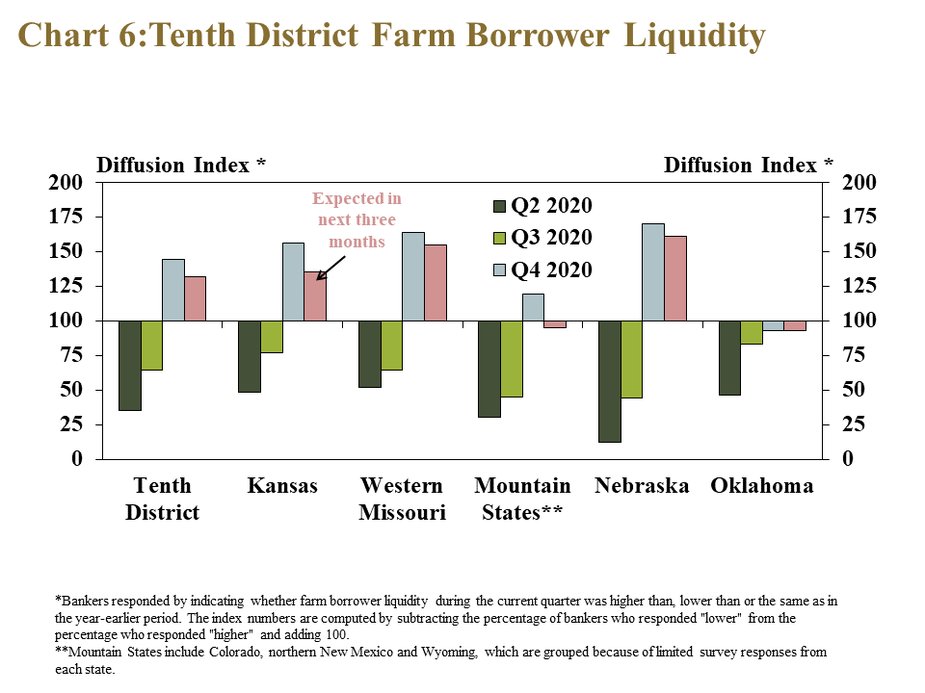

Much like farm income, borrower liquidity rebounded notably in all states except Oklahoma and the Mountain States. With improvement in cash flows and incomes, a majority of bankers in the region reported that farm borrower liquidity was higher than a year ago and that they expected conditions to remain similar in the next quarter (Chart 6). However, a majority of bankers in Oklahoma and the Mountain States indicated that liquidity was slightly less than the previous year

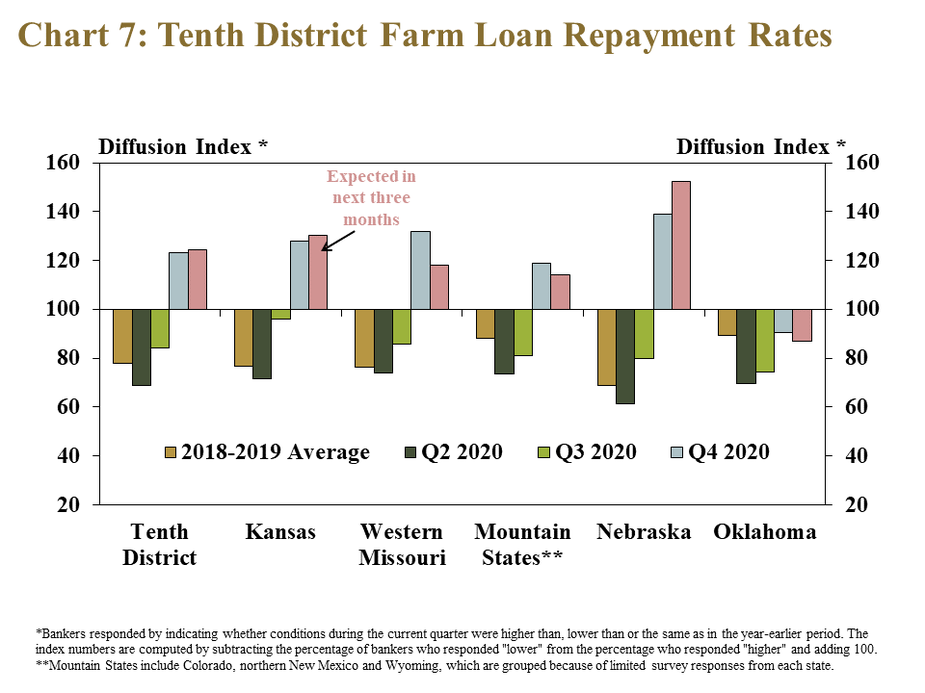

Better financial positions at the end of 2020 improved the ability of borrowers in most states to make loan payments. However, while the pace of deterioration slowed from previous quarters, the rate of loan repayment in Oklahoma continued to decline (Chart 7). Similar to other financial indicators, bankers were less optimistic about farm loan repayment rates in the most western and southern states of the District.

Farmland Values and Interest Rates

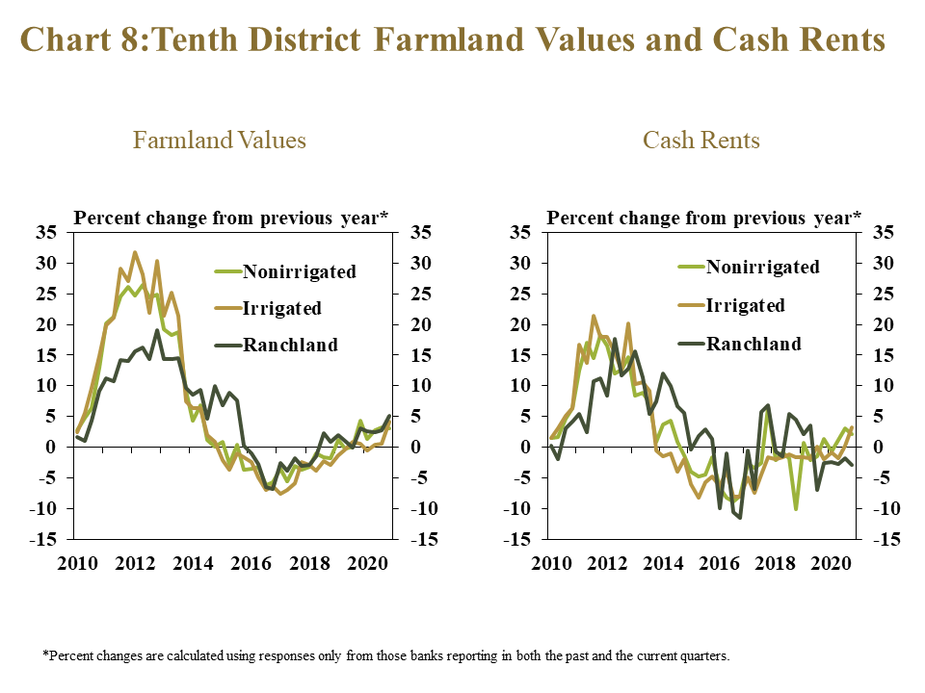

Alongside improved prospects for farm finances, an increase in farmland values across the region provided additional support to the sector. The value of all types of land increased an average of 4% from a year ago, the highest average increase across all land types in any quarter since 2014 (Chart 8). Cash rents for nonirrigated and irrigated cropland also increased, but at a slightly slower pace than the value of the land, and cash rents on ranchland continued to ease.

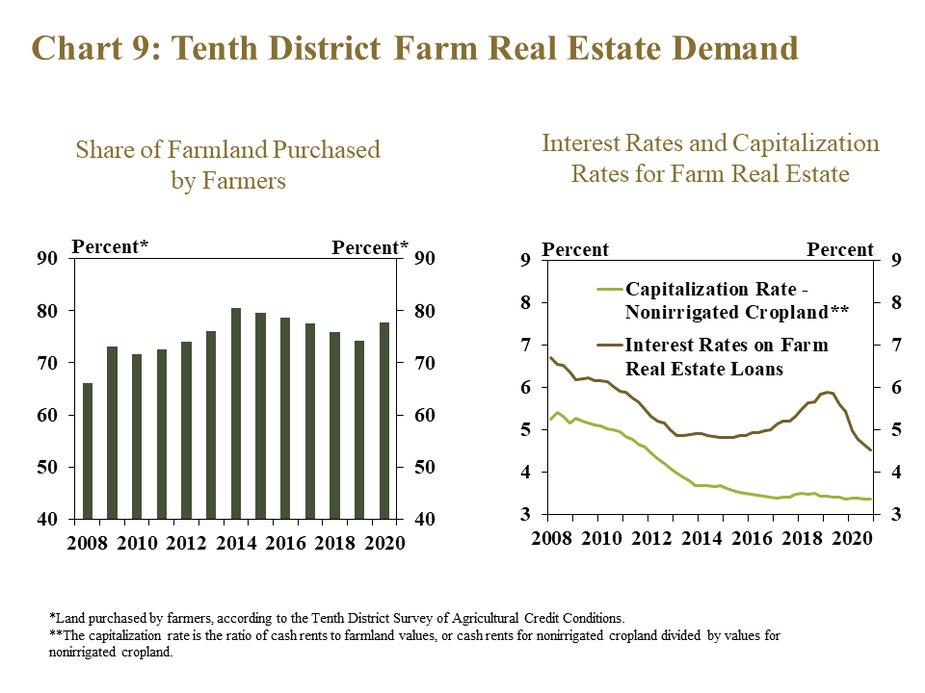

A decrease in interest rates and a modest increase in demand for farmland strengthened farm real estate markets. Demand for farmland increased, with producers accounting for a slightly higher share of land purchases than the prior two years (Chart 9). Lower interest rates likely also supported farm real estate markets by reducing financing costs and making farmland a more attractive investment opportunity. Interest rates continued to decline in the fourth quarter at a faster pace than the return to farmland ownership, or capitalization rate, suggesting a relatively greater incentive to own land and generate returns through leasing.

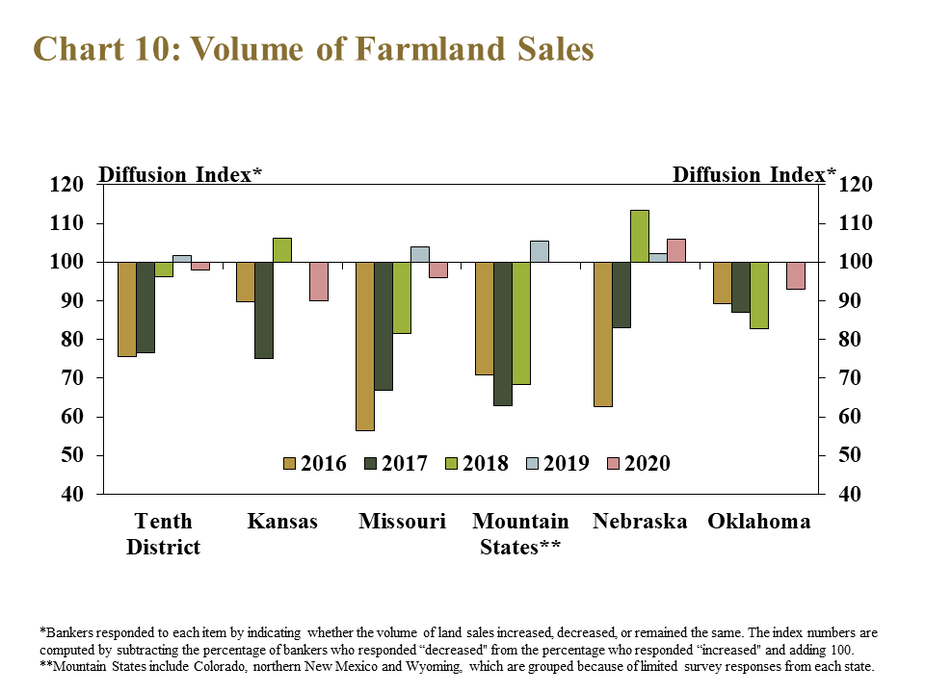

Agricultural real estate markets also were supported by a slightly lower volume of farmland sales in most states. Compared with a year ago, the volume of farmland sales declined slightly in the region overall and decreased or remained steady in all states except Nebraska (Chart 10). Fewer sales have limited the supply of farmland on the market and have put upward pressure on prices that buyers have been willing to pay.

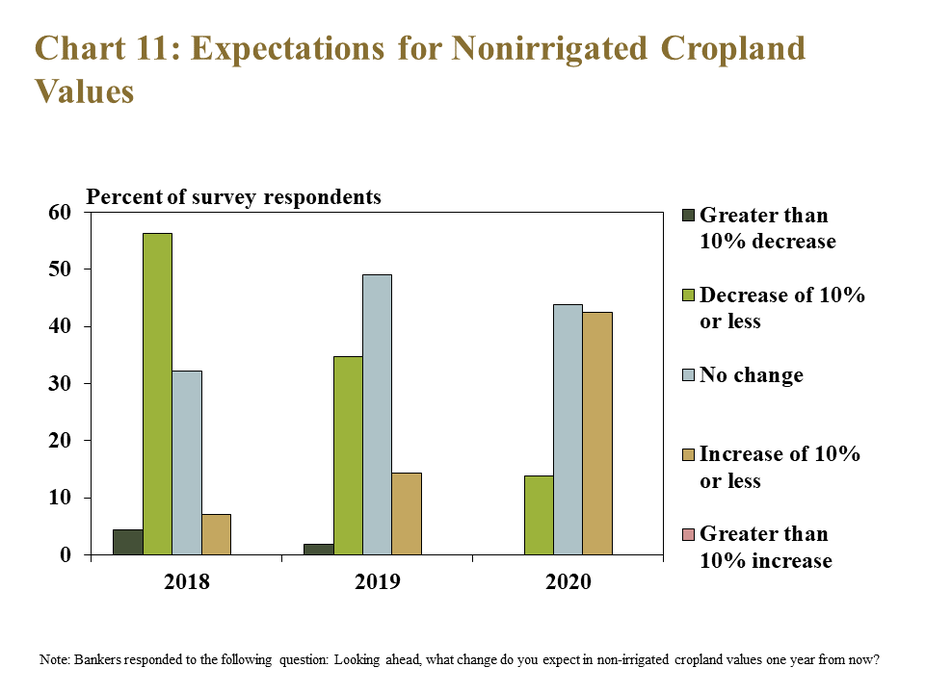

The combination of factors supporting farm real estate markets led to a notably more optimistic outlook for farmland values than in previous years. Less than 15% of bankers expected nonirrigated cropland values to decline in the next year, while over 40% expected an increase (Chart 11). The outlook at the end of 2020 was in stark contrast to previous years when a similar share expected values to decline.

Conclusion

Increases in commodity prices at the end of 2020 and robust support from government payments boosted economic conditions in the agricultural sector in the fourth quarter. A majority of bankers in the District indicated that farm income was higher than a year ago for the first time in eight years, boosting liquidity and loan repayment capacity, and providing renewed support for farm real estate. Overall, agricultural conditions in the first quarter of 2021 in the Kansas City Fed region were poised to remain strong for the first time since 2013.

________________________________________________________________________

Banker Comments from the Tenth District

“Large areas of drought hindered production. Alfalfa production was nearly half of historical amounts and numerous acres of corn were enrolled in Prevent Plant programs.” – Southeast Colorado

“Most of our ag borrowers are pretty much going to sit tight and wait for COVID-19 to pass before making any large monetary decisions.” – Northern Colorado

“Regional ag economic conditions appear to be unstable, with uncertainty of continued market volatility as a result of administrative change, COVID -19, and current drought conditions.” – Northern Wyoming

“Higher grain prices may lead to more pre-harvest crop sales, but higher feed costs for livestock production.” – Central Kansas

“Direct payments have been beneficial and commodity prices have been going up substantially, which certainly benefits those who stored grain.” – Northeast Kansas

“We are in an extremely dry area at this point in time. Yields have been good for the past several years and current prices are good, but if the dry weather continues it will have a grave impact on this community.” – Northwest Kansas

“Better than expected yields in our area coupled with much better than anticipated commodity prices has brightened the ag sector outlook.” – Central Missouri

“With the CFAP payments and the increase of commodity prices, gross farm income will be quite a bit more for 2020 than previous years and real estate sales have increased significantly over the last 45 days.” – Southwest Missouri

“Between all of the government payments and unprecedented harvest rally in grains, even marginal borrowers are showing at least modest financial gains for 2020 and low interest rates are fueling a bump in land prices.” – Northeast Nebraska

“If dry conditions persist into spring and early summer, ranch carrying capacities will be materially impacted.” – Northwest Nebraska

“I think there will be only a few borrowers with higher-than-expected farm income. We rely heavily in this area on cattle prices, which are lower than they were a year ago.” – Southeast Oklahoma

“COVID-19 relief payments to farmers and ranchers were well received and needed. Grain price improvement was beneficial to about half of our farmers.” – Northern Oklahoma

A total of 163 banks responded to the Fourth Quarter Survey of Agricultural Credit Conditions in the Tenth Federal Reserve District—an area that includes Colorado, Kansas, Nebraska, Oklahoma, Wyoming, the northern half of New Mexico and the western third of Missouri. Please refer questions to Nathan Kauffman, economist or Ty Kreitman, assistant economist at 1-800-333-1040.

The views expressed in this article are those of the authors and do not necessarily reflect the views of the Federal Reserve Bank of Kansas City or the Federal Reserve System.

Authors

Nate Kauffman

Senior Vice President, Economist, and Omaha Branch Executive; Executive Director of the Center for Agriculture and the Economy