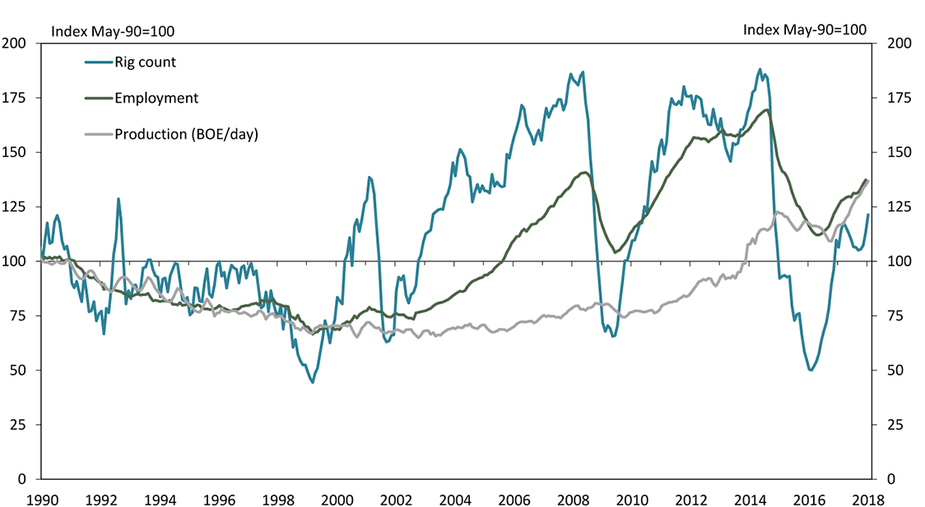

Oklahoma oil production, after dropping more than 20 percent in 2015, rebounded to an all-time high in December 2017 and has continued to grow rapidly in 2018. The state’s natural gas production also is at a record high. Yet the number of active oil and gas rigs remains almost 40 percent below the level of late 2014—despite solid increases over the past year—and oil and gas jobs in the state remain almost 20 percent below their previous peak. The oil and gas sector nationwide in recent years has experienced a similar surge in output per rig and worker. Indeed, from 2012 to 2017, productivity in the U.S. oil and gas extraction sector more than doubled.

Only rarely have other sectors of the economy experienced such rapid productivity gains. Analyzing what happened in those sectors in the years that followed may provide insights into the future of the oil and gas industry in the United States and Oklahoma. This edition of the Oklahoma Economist looks first at some of the data and factors behind the recent rise in U.S. oil and gas productivity. It then identifies other industries that have experienced similar surges in productivity, and what happened to their output, investment and employment in the decade that followed.

The boom in Oklahoma and U.S. oil and gas productivity

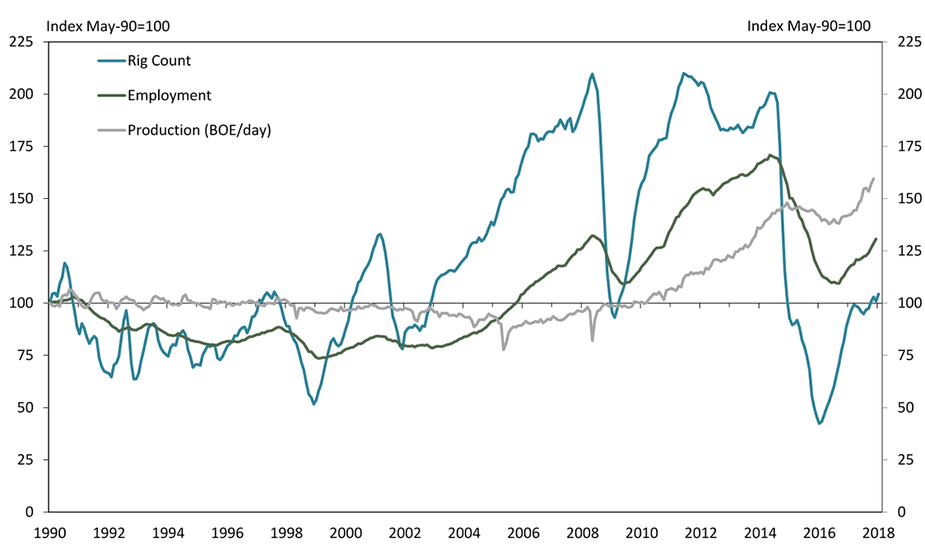

In both Oklahoma and the United States, total oil and gas production (measured on a barrels of oil equivalent basis, or BOE) is now about 10 percent higher than its previous record highs reached in mid-2015 (Charts 1 and 2).

Chart 1. Oklahoma oil and gas rig count, employment and production

Note: Employment is for total mining and logging, which in Oklahoma is almost completely oil and gas related. Production is shown as a three-month moving average.

Source: Baker Hughes, Energy Information Administration/Haver Analytics

Chart 2. U.S. oil and gas rig count, employment and production

Note: Employment is for NAICS 211, 213111 and 213112. Production is shown as a three-month moving average.

Source: Baker Hughes, Energy Information Administration/Haver Analytics

Despite this performance, rig counts and oil and gas employment in both the state and nation remain well below previous peaks. This contrasts with previous upturns in oil and gas activity in 2004-08 and 2010-14, when larger increases in rigs and workers were needed to push production higher.

While this recent surge in production per rig and per worker has been driven in part by a focus on more core areas of plays in recent years, which naturally are more productive, there have been a number of key drilling and technology enhancements. These include longer horizontal laterals, multiwell pad drilling, walking rig systems and increased proppant concentrations in hydraulic fracturing. Firms also are making greater use of data analytics to increase drilling accuracy and create process efficiencies._

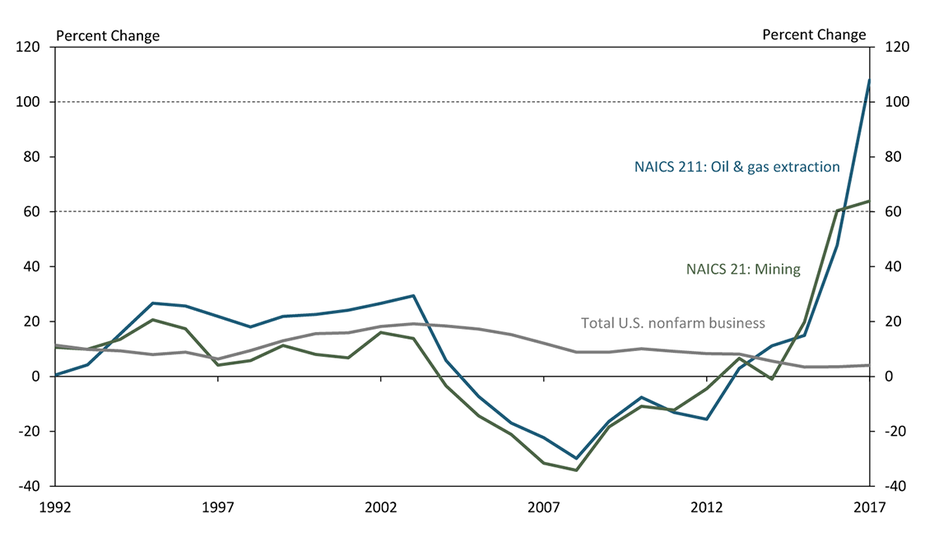

Based on national industry productivity data, official labor productivity growth (output per hour) in the U.S. oil and gas industry in recent years indeed has surged (Chart 3).

Chart 3. Industry labor productivity five year cumulative change

Source: Bureau of Labor Statistics/Haver Analytics, Author's calculations

From 2012 to 2017, output per hour more than doubled in the narrow oil and gas extraction industry, rising 108 percent. Firms in this industry, as defined by the Bureau of Labor Statistics, “operate and/or develop oil and gas field properties … up to the point of shipment from the producing property.”_ Productivity also rose more than 60 percent from 2011 to 2016 in the broader mining sector—which also includes “establishments primarily providing support services, on a contract or fee basis … for the extraction of oil and gas,” such as companies that provide drilling or completing services._ Most of the mining sector’s productivity growth in recent years has been in oil and gas extraction, while productivity growth in other types of mining (coal, metals, etc.) and in support services for mining (including for both oil and gas extraction and other types of mining), has been lower, although less detailed and timely data are available.

Past industries with similar productivity surges

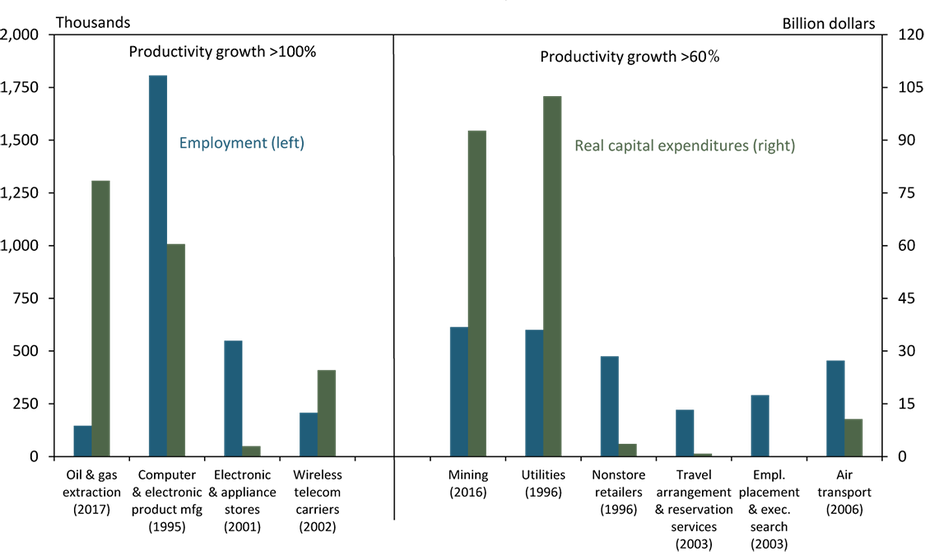

Only rarely have other U.S. industries experienced such rapid productivity growth. Detailed industry productivity data are available starting in 1987. Of 75 unique industries with data available, only three other than oil and gas extraction have had productivity double in a five-year period. Only five additional industries other than the broader mining sector have experienced greater than 60 percent growth in productivity in five years._

The other three sectors to have productivity double over a five-year period include: computer and electronic product manufacturing (reached in 1995), electronics and appliance stores (2001) and wireless telecommunications carriers, except satellite (2002). In terms of size, the oil and gas extraction industry has fewer jobs than these three industries did when they first doubled in productivity, but greater capital investment (Chart 4).

Chart 4. Size of industries in which five year productivity growth reached 100% or 60% since 1987

Note: Number in parenthesis denotes year in which five year productivity first reached the 100% or 60% threshold.

Source: U.S. Census Bureau, Bureau of Labor Statistics/Haver Analytics, Author's calculations

The other five sectors to have productivity rise more than 60 percent over a five-year period include: utilities (1996), nonstore retailers (1996), travel arrangement and reservation services (2003), employment placement agencies and executive search services (2003) and air transportation (2006). For comparison, the overall mining sector has more jobs than all of these industries did when they reached 60 percent productivity growth, and higher capital investment than all but utilities. The vast majority of mining sector investment is in oil and gas extraction, but employment is spread more evenly across oil and gas extraction (29 percent of mining sector employment), mining excluding oil and gas extraction (29 percent), and support activities for mining, including for oil and gas (42 percent).

Future output, investment, and jobs in high-productivity industries

All of the previous U.S. industries to experience a rise of more than 60 percent in productivity over a five-year period first reached those peaks more than 10 years ago. Thus, unlike for the oil and gas industry at this stage, data exist on what happened to output, investment and employment in those industries in the decade following their productivity surge.

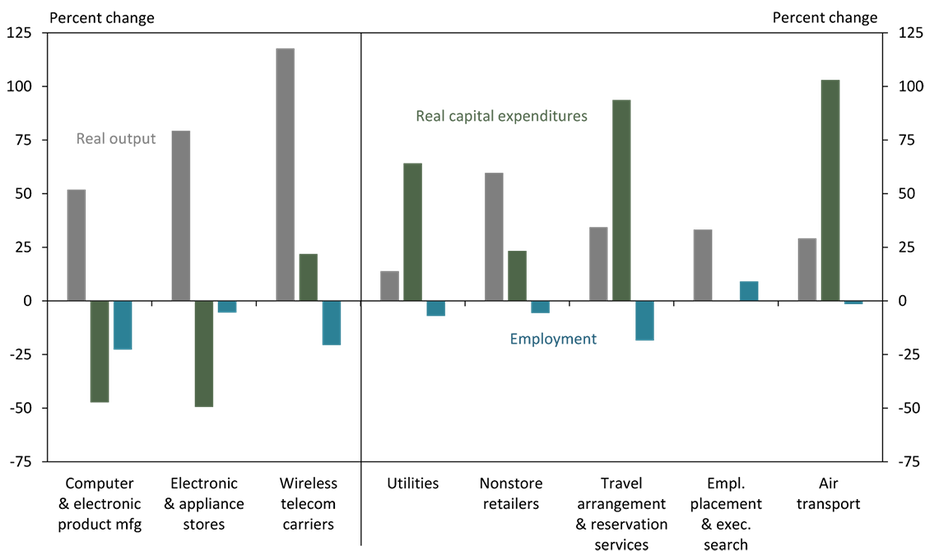

In all eight of the past industries to experience rapid productivity gains—and as might be expected—output (or production) rose further in the following decade, in most cases significantly so (Chart 5).

Chart 5. Change in output, investment and employment 10 years after productivity surge

Source: U.S. Census Bureau, Bureau of Economic Analysis, Bureau of Labor Statistics/Haver Analytics, Author's calculations

In the three industries in which productivity doubled in the previous five years, output grew more than 50 percent over the next 10 years. Among the five industries with slightly smaller productivity growth, output grew more than 25 percent in all but one.

In terms of the capital investment needed to boost future output in those industries, the trends are more mixed. Future capital investment rose in all industries experiencing between 60 and 100 percent productivity gains for which data are available (not available for employment placement and executive search industry). However, in two of the three sectors in which productivity rose more than 100 percent, investment fell in the following decade, despite sizable increases in output, and rose only moderately relative to huge output gains in the wireless telecommunications industry.

Future employment trends were more uniformly negative across the eight industries. Only one industry added jobs in the following decade—the employment placement and executive search industry—and in that case by less than 10 percent. Jobs fell in the other seven industries, and dropped by more than 20 percent in two of the three industries in which productivity doubled—computer and electronic product manufacturing and wireless telecommunications carriers.

Summary and implications

The Oklahoma and U.S. oil and gas industries have experienced historic productivity growth since 2012. Only a few other industries in recent decades have experienced such rapid growth in output per hour. Of those, all continued to increase output in the decade that followed, in many cases significantly, and most also increased capital investment. However, employment fell in almost all of them, in two cases by more than 20 percent.

These past examples suggest the outlook in the next decade for Oklahoma and U.S. oil and gas production could be quite positive, but the outlooks for oil and gas investment and employment may be more uncertain. As such, tax revenues related to oil and gas production may benefit in the years ahead, while taxes on investment or incomes and sales in areas heavily concentrated in oil and gas activity may be more at risk. This is an important consideration since oil and gas is the highest-paying industry to experience such rapid productivity growth._ If fewer resources are needed to increase oil and gas production over the next decade than in the past, affected areas may need to intensify efforts to diversify their economies into other industries that could use some of the workers and capital currently allocated to the oil and gas industry. At the same time, if production of oil and gas continues to rise, increased investment and workers in midstream and downstream energy businesses may be needed to move the increased production out of producing areas.

However, several factors make the oil and gas industry somewhat different from past industries that experienced rapid productivity gains, and thus future outcomes also may differ. Oil and gas is a commodity industry, and thus generally more susceptible to wide positive and negative swings in prices and activity. Somewhat related, it is also an industry with a sizable cartel, OPEC, which can affect production levels of producing countries across the world. As such, future production trends could be considerably higher—or lower—than in past high-productivity industries. In addition, the part of the oil and gas industry that employs the most workers—contract support services for oil and gas extraction—has experienced slower productivity growth than oil and gas producers. As such, that segment’s future employment risks may be lower.

______________________________________________________________________________

Endnotes

-

1

See, for example, “Technology and efficiency gains have boosted the oil industry,” Daily Oklahoman, May 20, 2018. External Linkhttps://newsok.com/article/5595139/technology-and-efficiency-gains-have-boosted-the-oil-industry

-

2

The NAICS code for “Oil & Gas Extraction” is 211. This subsector includes the production of crude petroleum, the mining and extraction of oil from oil shale and oil sands and the production of natural gas, sulfur recovery from natural gas and recovery of hydrocarbon liquids.

-

3

.

In addition to “Oil & Gas Extraction” (NAICS 211), the “Mining” sector (NAICS 21) includes the subsectors 213111: “Drilling Oil & Gas Wells” and 213112: “Support Activities for Oil & Gas Operations.” It also includes “Mining, excluding oil and gas” (NAICS 212), such as for coal or metals, and “Support Activities for Mining, excluding oil and gas” (NAICS 213113-5). Including the broader mining sector in the analysis can provide more context for the overall oil and gas industry.

-

4

Comparison industries include all three-digit NAICS industries for which there are data, along with four- or five-digit NAICS industries in cases where three-digit data are not available.

-

5

Average annual pay in NAICS 211: Oil & Gas Extraction exceeded $160,000 in 2016, more than $40,000 higher than in any other high-productivity growth industry, and in some cases more than $100,000 higher.