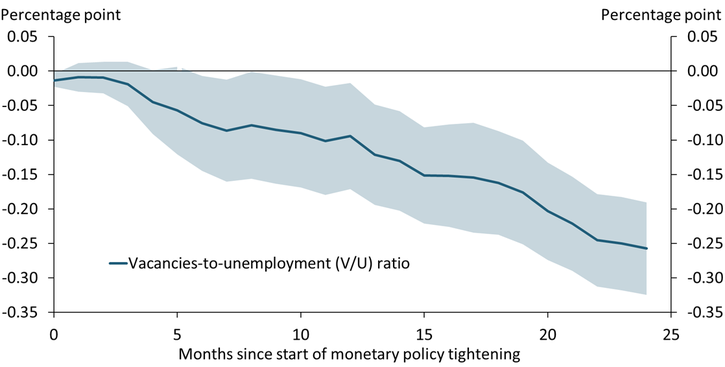

Notes: The chart shows the cumulative effect of a surprise hike in the federal funds rate, coded as a binary variable from Romer and Romer (External Link2023), on the job vacancies-to-unemployment ratio. Monetary policy surprises are narratively identified based on historical minutes and transcripts of Federal Reserve policy meetings. Shaded areas represent one-standard-error confidence bands.

Sources: U.S. Bureau of Labor Statistics (Haver Analytics), Romer and Romer (External Link2023), Barnichon (External Link2010), and author’s calculations.

Historic evidence since 1951 suggests that labor markets respond only slowly to tighter monetary policy. After a surprise hike in the federal funds rate, the vacancies-to-unemployment (V/U) ratio, a popular measure of labor market tightness, declines by an estimated 0.26 percentage points over 24 months. This slow cooling of the labor market is in line with the current tightening cycle. Since the Federal Reserve started raising the policy rate in March 2022, the V/U ratio has only declined from about 1.9 to 1.5 so far and is still well above the pre-pandemic average of about 0.8.

See more research from Charting the Economy.